Bunker Ammonia: Rapid Cross-Sector Progress from Industry, Government, Finance, and Class Societies

By on August 09, 2019

The maritime industry has been engaged in a frenzy of research since April 2018, when the International Maritime Organization (IMO) announced its Initial GHG Strategy mandating a 50% reduction in shipping’s emissions by 2050.

On one hand, some industry players still believe that “there is no known technology today by which we could reach the 2050 target.” On the other hand, “2030, not 2050, must become the target, as the approximately 20-year lifetime of ships means that steps will need to be in place by then.” (These quotes are from an article that surveys industry actors on the difference between meeting IMO targets in 2020 and in 2050, titled “Shipping looks beyond the sulphur cap.”)

Industry leaders are now moving at remarkable speed to identify viable low-carbon propulsion technologies that can be demonstrated within the next few years, deployed in the next decade, and then adopted across the global industry, with infrastructure in place, at a scale sufficient to meet the IMO’s target in 2050. Chief among the carbon-free options are batteries, hydrogen, and ammonia:

Ammonia [is] regarded as compatible (in its liquid form) for existing infrastructure according to James Mitchell, manager global climate finance industry programmes at US-based Rocky Mountain Institute. “Ammonia is an easier fuel to transport, as well as having the right fuel density and being more compatible with existing infrastructures than other options.”

Riviera Maritime Media, Shipping looks beyond the sulphur cap, June 11, 2019

Since I last wrote about its two-stroke ammonia engine in January 2019, MAN Energy Solutions has been evaluating an ammonia fuel conditioning module with OEM Alfa Laval. Beyond technology development, three recent announcements illustrate the speed and depth of progress across a range of maritime stakeholders.

In the government sector, the UK has launched its Clean Maritime Plan, which identifies ammonia as one of its strategic “clean growth opportunities.” In finance, a coalition of 11 banks representing a shipping portfolio of around $100 billion has launched the Poseidon Principles to “redefine the role of banks in the maritime shipping sector.” And in the class societies, ABS has launched its Global Sustainability Center in Singapore, to analyze, certify, and validate alternative fuels and new technologies.

ABS Global Sustainability Center

ABS is one of the leading international class societies. It describes itself as providing “classification and technical advisory services” to the shipping and offshore industries, and being “committed to setting standards for safety and excellence in design and construction.”

In April 2019, ABS launched its Global Sustainability Center with the “mission to help maritime transition to a sustainable, lower emissions industry.”

According to its Chairman, President and CEO, Christopher J. Wiernicki:

“To facilitate the journey toward decarbonization targets, ABS established its Global Sustainability Center to coordinate initiatives that advance innovation and technology development focused on safety, practicality and the commercial viability of proposed solutions.”

Located in Singapore, the advanced facility is the flagship of ABS sustainability activities across the globe. The center is led by Gurinder Singh, ABS Director of Global Sustainability, and includes a team of professionals with diverse backgrounds and expertise, supported by the worldwide ABS organization.

ABS press release, ABS Launches Global Sustainability Center to Help Industry Transition to a Low-Carbon Economy, April 7, 2019

According to ABS’s announcement, the Global Sustainability Center will:

- Study “the viability of alternative fuels and new energy sources;”

- Analyze “de-carbonization pathways” that deliver the IMO’s targets within the context of anticipated growth in global trade;

- Use digitization to “simplify transactions and increase operational efficiency;” and

- Certify, verify, and validate new technologies.

Later this month, Gurinder Singh will be speaking at “Ammonia = Hydrogen 2.0,” the inaugural conference of the Ammonia Energy Association–Australia, held in Clayton, VIC, August 22-23. The title of his talk is “Green ammonia as marine bunker fuel.”

The Poseidon Principles

Launched in June 2019, the Poseidon Principles is a “new type of climate change agreement … the first global, sector-wide, and self-governing climate alignment agreement among financial institutions.”

Its founding signatories include eleven banks representing $100 billion, and it was drafted over a period of 18 months by a coalition of class societies (Lloyds Register), ship owners and traders (Maersk, Cargill, Euronav), and “leading civil society organizations” (Global Maritime Forum, Rocky Mountain Institute, and University College London Energy Institute). The signatory banks are Citigroup, Societe Generale, DNB, ABN Amro, Amsterdam Trade Bank, Credit Agricole CIB, Danish Ship Finance, Danske Bank, DVB, ING, and Nordea.

In simple terms, the Poseidon Principles describes four principles:

- Assessment: signatories will use a specific methodology to measure the “climate alignment” of their portfolio, defined as the “carbon intensity relative to established decarbonization pathways”

- Accountability: signatories will assess and report climate alignment using unbiased information, following “mandatory standards established by the IMO” and relying on “classification societies or other IMO-recognized organizations.”

- Enforcement: “standardized covenant clauses will be made contractual” for all new business.

- Transparency: “Portfolio climate alignment scores will be published on an annual basis.”

In its announcement of this new agreement, the Rocky Mountain Institute addresses a cause of failure for many well-intentioned climate actions:

Overcoming Competition Through Scale

If a single bank tries to align itself with a climate agreement, it may have to rebalance its portfolio away from carbon-intensive industries. If it chooses to maintain its role in carbon-intensive industries, it runs a significant risk of losing clients and projects to competitors. Either way, the world goes on largely as it was.The first key innovation of the Poseidon Principles is to overcome this challenge by achieving collective action at a global scale. Currently, the Principles represent around $100 billion of the global shipping portfolio. This is expected to grow to cover a significant majority of the global shipping loan book in the future. With scale comes both safety in numbers and an unprecedented ability to require clients to make short- and long-term cuts to emissions in exchange for access to lending.

Rocky Mountain Institute, The Poseidon Principles: A Groundbreaking New Formula for Navigating Decarbonization, June 17, 2019

Lending is the business that the Poseidon Principles hopes to change and, beyond shipping, the architects of the program hope that it can later be adapted to drive decarbonization in other hard-to-abate industries.

Capital-intensive assets like ships, planes, power stations, and manufacturing facilities are vital to our modern economy, yet today account for an incredible 78 percent of global GHG emissions. In order to hold global warming well below 2°C as the Paris Agreement requires, we will need to see the assets that underpin our economy completely transformed by mid-century.

Rocky Mountain Institute, The Poseidon Principles: A Groundbreaking New Formula for Navigating Decarbonization, June 17, 2019

The UK’s Clean Maritime Plan

As I wrote in February 2019, the UK’s Department for Transport (DfT) called for the launch of ammonia / hydrogen powered vessels within 5-15 years, in its Maritime 2050 report.

Now, the DfT has released its more detailed Clean Maritime Plan, in which it doubles-down on its commitment to ammonia as a viable option to be developed and demonstrated, due to its strategic importance to economic growth in the UK.

The research identified hydrogen and ammonia production technologies as offering the most significant potential economic benefits to the UK … The UK also has a strong competitive position in relation to ammonia production technologies. In particular, the UK has a strong domestic position for ammonia catalyst supply, and ammonia-based fertiliser is produced in volume in the UK. This is important because catalyst supply is a high-value part of the supply chain.

UK Department for Transport, Clean Maritime Plan, July 2019

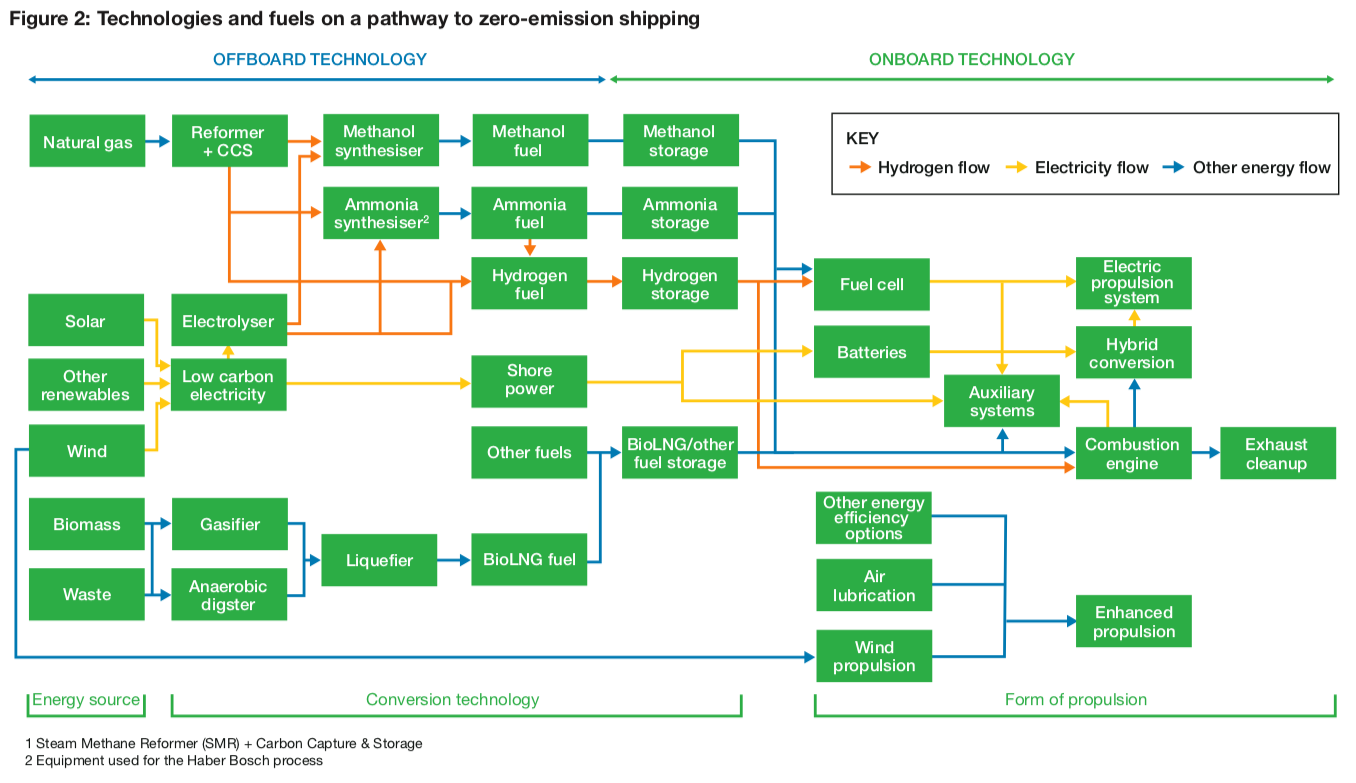

The Clean Maritime Plan assesses a broad range of technologies and fuels on the “pathway to zero-emission shipping.” Despite “substantial uncertainty,” its analysis of carbon-free and synthetic fuels concludes that “ammonia is estimated to be more cost-effective than methanol or hydrogen for most ship types.”

One of the specific government commitments disclosed in the Clean Maritime Plan is “Providing seed funding to contribute to the establishment of MarRI-UK,” which it describes as a “a hub to co-ordinate research and innovation activities in the field of zero emission shipping.”

The intention of this workstream would be to initially support zero emission projects generally in the early (3 – 7) TRL [technology readiness level] stages. Where possible, these projects would be aligned with technologies in which the UK has been identified as having a competitive advantage. Research commissioned by the Government assessed the UK’s competitiveness in 11 key clean maritime technologies and found that the UK has the strongest competitive advantage in hydrogen and ammonia production technologies, on-board batteries and electric engines.

UK Department for Transport, Clean Maritime Plan, July 2019

And the winner is …

All segments of the shipping industry are now engaged on a steep learning curve and committed to moving quickly, but the industry hasn’t reached a consensus — most importantly, perhaps, with regards to the role of LNG as a transition fuel.

(LNG is very important today because it is a “low-sulphur” fuel that helps the industry to meet the IMO’s 2020 target: a 0.5% sulphur cap. However, LNG is only a “low-carbon” fuel relative to heavy fuel oil; LNG cannot possibly deliver the 50% GHG reduction mandated by the IMO because it contains far too much carbon.)

There is a conflict between the need for long-term solutions to be deployed in the next decade, and the need for short-term operating profits in the meantime. This was perfectly illustrated by two contrasting quotes in a recent article:

Andrea Morgante, the vice president in charge of business development [at Wärtsilä], believes hydrogen or ammonia could become the dominant fuel for the sector in the coming decades.

However it will take around a decade for production to scale up … In the meantime, Wartsila is putting its money on liquid natural gas (LNG) … “Our message is that we cannot wait for new technologies to become available to start changing,” Morgante said.

“We need to start having a serious conversation that [hydrogen and ammonia] are the only two options, and then get on with getting the investment in,” says [Tristan Smith, an expert in low-carbon shipping at UCL]. He worries that switching to LNG could lock the industry on a path where it is burning fossil fuels well into the future.

City A.M., Set sail for the 1700s: Why the shipping industry is returning to technology from the history books, July 21, 2019

Of course, the industry stakeholders who will ultimately decide between these two perspectives are the banks, because they will provide the financing to build new ships and bunkering infrastructure, and they will determine which technologies are “bankable.” For this reason, the Poseidon Principles represent a powerful force for change within the industry.